The present study, conducted by modefinance, aims to provide a snapshot of the health of companies by analyzing the semi-annual financial statements of over 14 thousand listed companies globally.

The analysis sample

The considered sample includes businesses, categorized by geographic area and macro-sector, with at least 10 million in revenue and available data for 2022 and 2023. In particular, divisions were made for continents and macro-regions: Europe, the Middle East, Central and Far East Asia, Oceania, Africa, South America, Central America, and North America.

Macro-sectors were selected based on data availability and their relevance to the sample:

- Agriculture, forestry, and fishing

- Extraction of minerals from quarries and mines

- Manufacturing activities

- Provision of electricity, gas, steam, and air conditioning

- Water supply; sewerage, waste management, and remediation activities

- Construction

- Wholesale and retail trade; repair of motor vehicles and motorcycles

- Transportation and storage

- Accommodation and food service activities

- Information and communication services

- Financial and insurance activities

- Real estate activities

- Professional, scientific, and technical activities

- Public administration and defense; compulsory social security

- Education

- Health and social care

- Arts, sports, entertainment, and recreation activities

- Other service activities.

The methodology and the objective

To obtain the most up-to-date picture of the trend, the semi-annual data of the sample companies were analyzed, with a particular focus on turnover and EBITDA. This involved comparing last year’s data with the latest available for 2023 to determine the variation between these values, both for a comparison between geographical areas and for different sectors. Given the objective and the wide variety of businesses considered (ranging from SMEs to multinational corporations), the decision was made not to consider aggregated data but to examine variations for each individual company. Median values for the corresponding peer group were then calculated from these individual company variations. This approach aims to promote greater comparability across sectors and geographical areas.

Observations

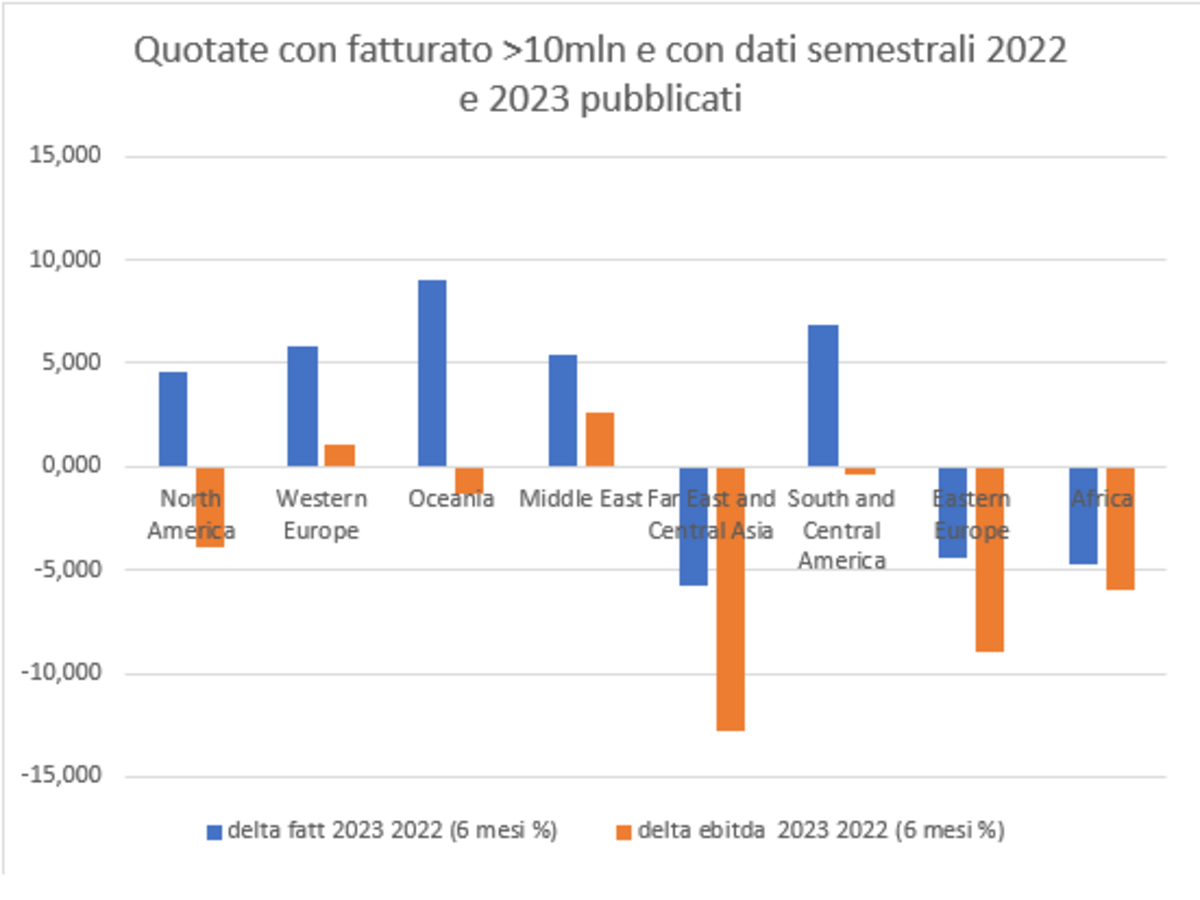

From a macroeconomic perspective, there are evident geographical differences. Firstly, companies in Western Europe and the Middle East show resilience in their results (+5.7% and +5.4% respectively in Δturnover). Oceania exhibits very positive outcomes, with a 9% growth in turnover compared to the first half of 2022.

On the other hand, companies in South America, Central America, and North America display mixed signals, with an overall increase in turnover accompanied by a growing level of indebtedness. Additionally, there are some territories experiencing a general decline, both in Δturnover and ΔEBITDA, including Eastern Europe, Africa, and Central Asia.

{kind=link}

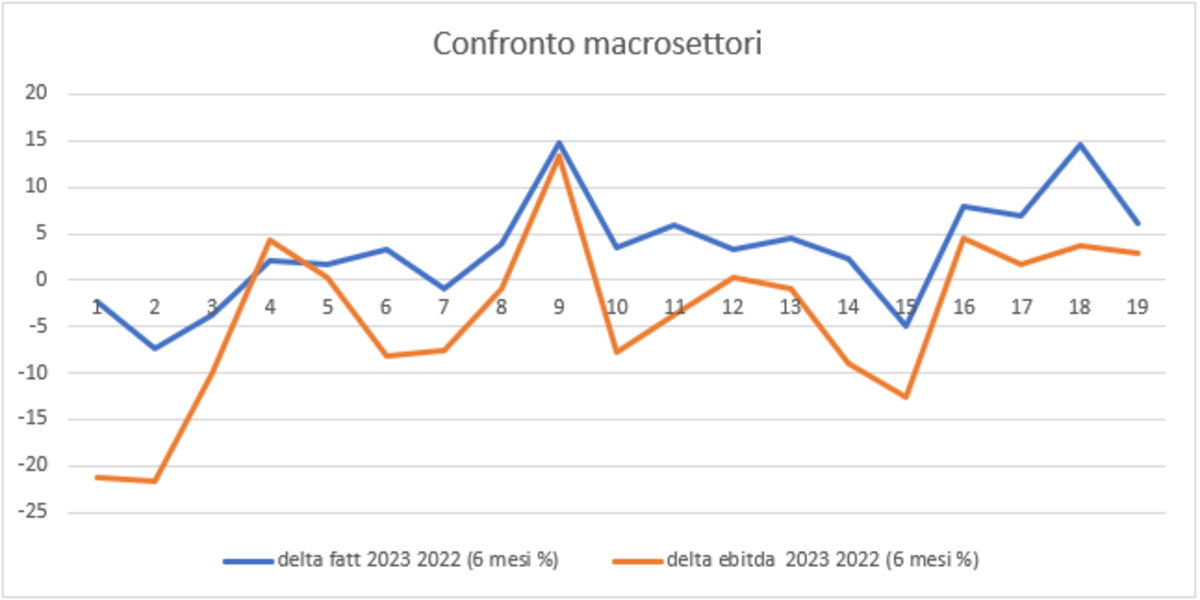

At the sectoral level, there are noticeable…

In particular, raw materials, the mining sector, and agriculture show negative variations in both turnover and profitability. Among these, the agriculture sector is the weakest, demonstrating a -2.3% change in turnover and a -21.2% change in EBITDA.

In slight decline, but more moderate, are construction, transportation, and the wholesale and retail trade segment, as well as the administrative sector. The construction sector, moreover, exhibits different trends in profitability and margins, with a 2.3% increase in turnover but a significant decrease in margins at -8.2%. These results have certainly been influenced by the effects of the Superbonus and various construction incentives promoted in recent years. At the same time, the dragging effect resulting from the halt in construction activities during the pandemic period has also had an impact. This is evident both in Italy and on a broader scale.

Experiencing a strong acceleration are accommodation and food service activities (+14.6% change in turnover and +13.3% change in EBITDA). It is significant that this sector has been one of the key drivers of the post-Covid economic recovery, following the severe restrictions that characterized the peak period of the pandemic.

Companies active in the energy sector (electricity, gas, steam, and air conditioning supply) are, on the other hand, substantially in line with previous trends, showing a steady growth in profitability and margins, at 2.1% and 4.3%, respectively.

{kind=link}