Why should companies claim an ESG assessment?

ESG ratings, as a validation of a theoretical approach to the concept of sustainability, should be adopted in conjunction with a sustainable transformation, to obtain a 360° evaluation as a purely financial value.

Moreover, companies that comply with environmental, social, and governance responsibility criteria are more attractive for the financial institutions, finding it easier to access credit and, at the same time, achieving a competitive advantage.

For the market, it is nowadays necessary to flank the credit ratings of certified rating agencies with a sustainability assessment. One of our previous articles already introduced the parameters used by modefinance for the three ESG criteria's assessment: despite the lack of univocal data and standard models that unite the sustainability assessments carried out by Rating Agencies and helpful to financial institutions, modefinance's financial analysts developed advanced modeling that allow them to conduct an extensive investigation of the three E, S and G pillars, based on methodological and statistical results. The subsequent assessment reveals the company's approach to sustainability and whether the latter is able to deal with risks related to environmental emergencies, or if the company is able to comply with existing regulations regarding social conduct and governance.

In this context, it becomes crucial for the financial analyst to understand how the company incorporates risks and opportunities into its strategic decision; it therefore becomes important to analyze the path that led to the definition of the current regulations governing ESG criteria’s integration within corporate strategy, considering their risks and opportunities.

The evolution of ESG regulation

- Reorientation of capital flows towards sustainable investments;

- Integrate sustainability into risk management;

- Promote transparency and the long term.

As a result, in the same year, the ECB introduced the 'ECB Guide on climate-related and environmental risk'. The document outlines the main actions to properly integrate climate-related and environmental risks into the strategy and governance of significant banks, and verify their status through two questionnaires concerning the assessment and the strategic plan. In 2021, the ECB then published a document identifying the positioning of SSM banks, and the following year it conducted the first Stress Test exercise to identify the banks' level of resilience to the possible impacts of climate-related risks.

Let’s focus on Italy: in April 2022, the Bank of Italy prepared the document 'Supervisory Expectations' focused on the risks associated with the sustainable transformation process. The disclosure concerns both corporates and the so-called 'less significant banks' and integrates these risks within corporate strategies, governance, and control systems, in the context of risk management and the disclosure of financial intermediaries and institutions.

Based on European Commission’s proposal, Bank of Italy’s regulation addresses financial intermediaries with an explicit request to integrate climate and environmental risk factors into their strategies. The paper clarifies how the effects of climate change, biodiversity, and ecosystem degradation can negatively affect economic and business performance if neglected.

The proposed material, even though addressed to financial institutions, also proves to be fundamental to define the role of the Rating Agency and sustainability assessment: the traditional credit rating takes into account the economic and financial variables that affect companies and the context in which they operate, such as the reference sector and the country in which they operate. Likewise, ESG assessments must consider the context as a variable of the risks associated with sustainable transformation. modefinance’s view Exposure vs. Management has been developed from this approach, whereby a company is assessed according to its level of awareness and, consequently, the framework of active policies it puts in place to manage the issues.

Physical risk and transition risk

The Bank of Italy's 'Supervisory Expectations' document has identified and defined two categories of risk that Financial Institution must consider: we talk about physical risk and transition risk.

With the notion of physical risk we refer to the economic impact of the increased number of natural disasters, the latter being either ‘extreme’ or ‘chronic’.

Transition risk instead is defined as the economic impact of a company's activity to reduce Co2 emissions to favor the exploitation of renewable energies.

It becomes essential to complement the credit rating with an assessment of the impact that the company's sustainable transformation actions will have on the company itself and the stakeholders involved.

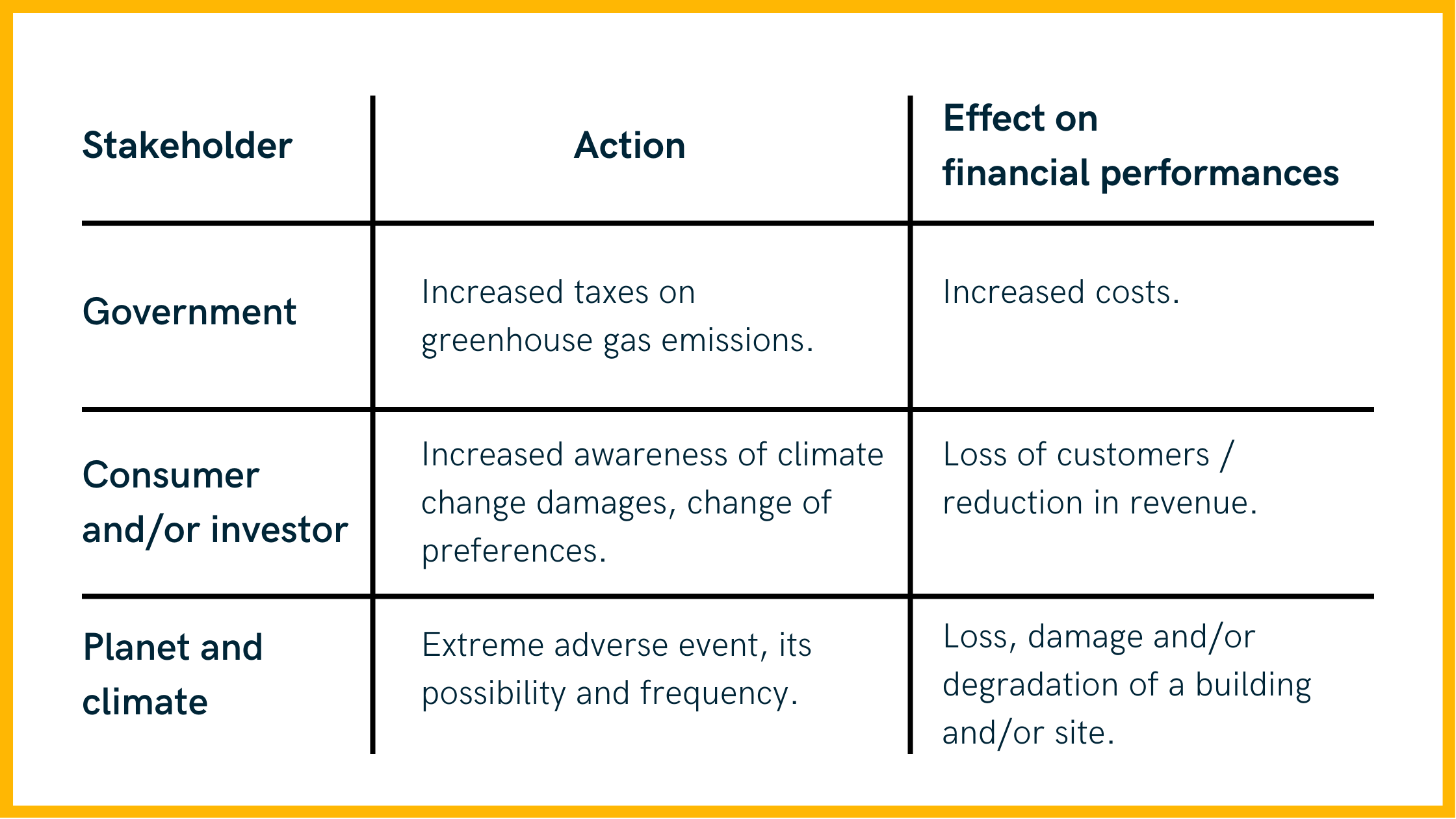

Furthermore, the Bank of Italy instructions pays particular attention to the above-mentioned cause-effect relationships, such as:

{kind=link}

In conclusion, it is crucial not to underestimate the importance of a targeted approach to assessing physical and transition risks. We considered it a priority to equip ourselves as soon as possible with advanced models that allow companies to know the impact that these risks may have at an economic and financial level on the conduct of their business, also considering what has been proposed by institutions, and based on what is likely to become a standard approach.

Moreover, the daily-based ongoing R&D embedded in modefinance’s mechanisms is evidencing that it is crucial to create advanced models capable of foreseeing the impact of climate and environmental risks for companies and stakeholders.

Firms, capital markets, small businesses are all involved in the ESG theme: the chance to obtain an ESG assessment, and it’s risks’ and opportunities’ awareness, will arise their growth opportunities within a sustainable future, key to everything we described so far.

Sustainability is increasingly becoming a synonym for survival in the marketplace, and one needs to take corrective action as soon as possible.