Fintech and BigData customer rating evaluation

More and more often we get a simple thus concrete question when we talk about partnerships and clients relations: “Will clients pay me or not? Will it be on time? How can I trust them?”.

Now apply this question to an entire portfolio. If that’s not enough, think about historical relationships, as a result of the economic crisis, without compliance guarantees on payment terms.Is there a solution?

Is there a reliable and systematic method for customer evaluation? Well, the answer is Yes.

That's simple: client’s evaluation has to be reliable, objective and distinguish good (healthy) and bad (risky) payers, without major margins of error. The evaluation should be systematic and applicable to the entire portfolio. One of the solutions is to develop a credit scoring model.

Requirements

{kind=link}

The model should be able to discriminate healthy and risky companies, starting from the elaboration of certain variables. This model must be easily applicable to the entire customer portfolio.

How to build a model

First of all, it is necessary to obtain financial information (e.e. financial statements and balance sheets) from a large group of active companies and a set of failed ones. You can use your own portfolio if wide and heterogeneous enough (i.e. with good sectoral, geographical and dimensional representation of the present and future business). Several info-providers have these information at affordable costs.

A good model always starts from the following three phases:

- Choose variables;

- Aggregate them (and how to develop the model);

- Validate.

How to choose the variables

The purpose here is to identify variables that have an intrinsic ability to separate healthy companies from risky and failed ones. Statistically, there are different techniques to do this, but to keep things simple let's rely on common sense.

To get a company’s health complete picture, we try to analyze all its fundamentals.

We will therefore have to create descriptive variables of:

- Solvency;

- Liquidity;

- Profitability;

- Interest coverage;

- Etc...

Solvency, for example. Let's create an indicator that measures the level of indebtedness of a company, on its own resources: total debts/equity. Common sense will suggest that the higher the level of relative indebtedness, the greater the riskiness of the company.

Some indicators could provide almost identical indications (in the jargon they are said to be related). In this case, to simplify the model, you can choose the most easily reproducible indicator on the entire portfolio.

Model development

{kind=link}

We mentioned in the previous step that, as a general rule, the more indebted a company, the more risky. Now we need to formalize this approach for all the indicators we want to consider in the model.

For example, we rate each indicator from 1 to 10. In our model, we must provide the possibility of giving a judgment from 1 to 10. “How do I know if a certain value for an indicator is good or bad?”. The two groups of companies help us: healthy and bankrupt. First of all, for each indicator, let's look at the values’ differences (maybe average) between healthy companies and failed companies.

In order to strengthen the model, this analysis should be carried out at the sector and country level: in fact, we can’t evaluate a leverage index of a heavy industry, compared to a service company.

Finally, how do we put together all the evaluations coming from each indicator? Different mathematical models are proposed in the literature. To keep things simple, a weighed sum will go just fine. Once again, you will ask: "Yes, but I weigh the same as I attribute them?".

As a general rule, you are right if the hierarchy of weights will be the following (with reference to the fundamental areas mentioned before):

- Solvency;

- Profitability;

- Liquidity;

- Interest coverage.

Well, at this point, the model is done, but the main question is: "will it work?"

Model validation

{kind=link}

Last, we get back to the two companies’ groups (which could be all or part of your portfolio).

We need to evaluate them with the model we developed. If the model gives a very low score to almost any failed business, and a higher score to the active ones, then we can say our model works. Conversely, something needs to be changed. Going back to judgments let’s us tune the variables’ weights and try again.

Conclusions

Does it seem like too much? A mammoth task? At a typical lesson on customer evaluation, we experiment the creation of a custom model: we divide participants into two groups, who will usually create their credit scoring model, starting from white Excel sheets, following all the described phases and with a minimum support by modefinance analysts.

The lesson itself enables them to analyze a company starting from the balance sheet, thus constructing the appropriate indicators (the same used in the model) and having critical evaluation’s notions.

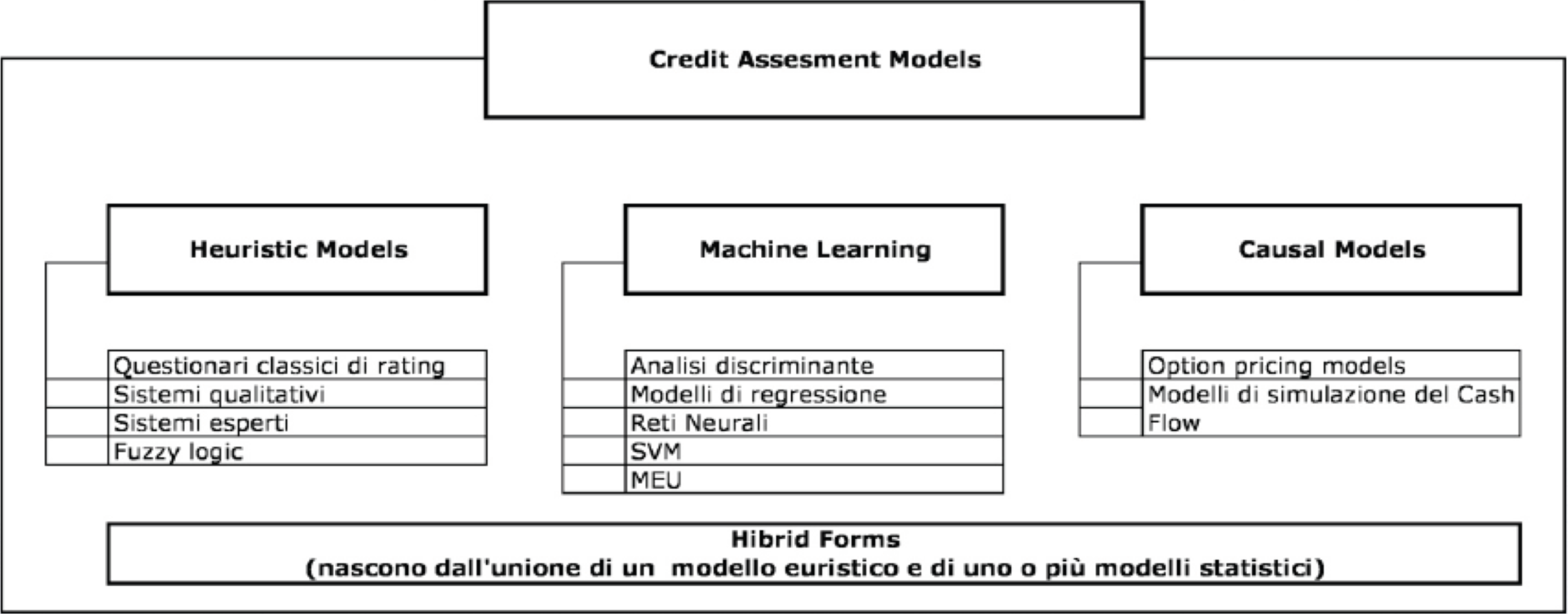

To be honest, nowadays the creation of Credit Scoring models involves considerably more complex elaborations, such as data mining process, multivariate statistical analysis, implementation of Machine Learning algorithms, etc.

However, the basic concepts underlying all this are substantially those described, which are, moreover, also those that allow us to understand whether more complex models work well or not.