Brief introduction

A few weeks ago we saw how to cut down times and cost of factoring due diligence process with oplon Risk Platform.

Today we'll deepen this topic, focusing on how to perform a credit risk analysis of the assignor and the debtors' portfolio in a few minutes, taking into account risk-adjusted metrics and real-time data.

oplon Risk Platform is designed to ensure the utmost flexibility in the development of your risk management policy. So said, modefinance is able to offer a tailored solution to better intercept your needs, developing custom folders, analysis tools and models (we talked about it here).

Prescreen analysis

Let’s start by the very beginning, i.e. by setting up the folders to be included in the platform.

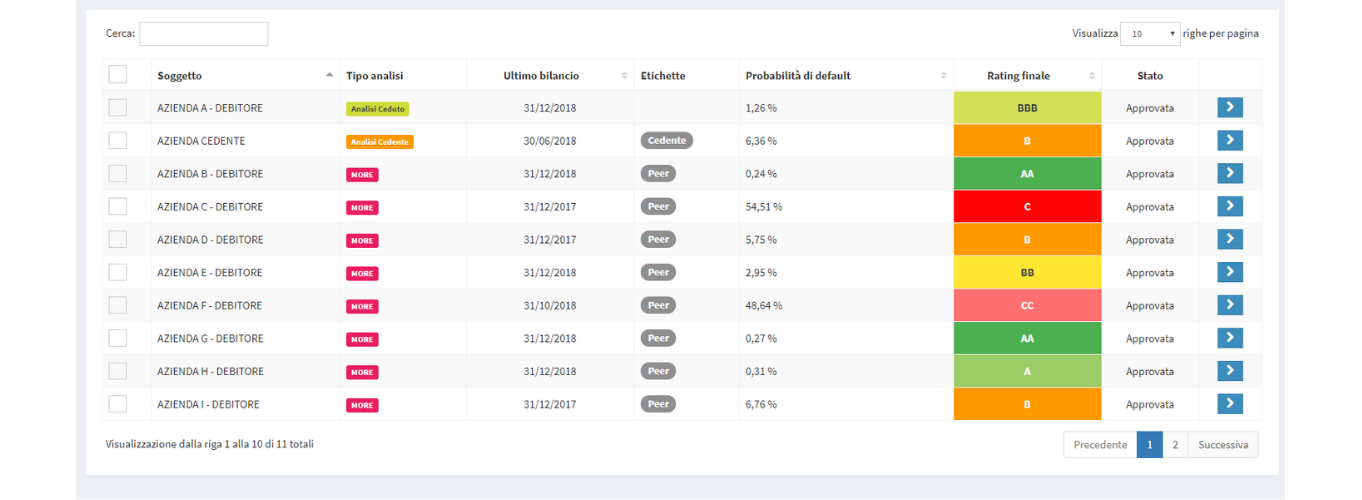

We opted for two folders: one dedicated to recourse factoring operations and the other one for operations without recourse. The case study we’re going to see is an example of a credit risk assessment of a recourse transaction.

Inside the folder we can perform different analyses on different counterparts. First of all, we’re going to perform a prescreen analysis of the assignor's creditworthiness in order to assess its eligibility to the factoring operation.

As already mentioned, all the tools and modules included in the platform are defined during the platform set-up. Except for MORE, which is modefinance’s scoring model. The model and applies the MORE methodology to calculates the company's credit score from the balance sheet data. For a more accurate evaluation, you can fine-tune the result by answering a multiple-choice questionnaire, that allows you to include in the creditworthiness analysis the qualitative factors.

{kind=link}

For a more accurate assessment, we also included in the analysis:

- the credit history evaluation model: it allows a point-in-time assessment of the customer's riskiness by including the assignor’s credit history provided by credit bureaus in the creditworthiness assessment;

- the forecasting model (ForST): it performs budget simulation on different growth scenarios, allowing to stress-test key variables in order to define the company's debt capacity.

The analysis process takes just a few minutes and leads to the definition of a final rating, which provides an indication of the assignor's eligibility to factoring operations.

The massive analysis

As part of the assignor’s creditworthiness analysis we can also include a pre-screening of the transferred portfolio using a massive analysis. The model allows you to calculate, by entering the VAT number only, the credit score and the probability of default of each debtor. The results of the massive analysis may affect the assignor’s credit score.

{kind=link}

The Portfolio Risk Analysis

Once the assignor's eligibility has been verified, it is possible to perform a much more in-depth analysis on the debtors’ portfolio in order to determine the factoring operation’s terms.

Let’s take a step back to the massive analysis model. Along with the VAT numbers, we can here enter the exposure amount of each debtor. It is not mandatory to include exposures to manage the massive analysis, but they are required to proceed with the portfolio risk analysis.

This is probably the most interesting feature. The model provides a portfolio evaluation on risk-adjusted measures, estimating the amount and the distribution of the expected losses and the Value at Risk. You can here verify which debtors contribute most to the VaR and get an estimation of the risk profile of the operation the most accurate and precise. The data of the portfolio risk analysis can be integrated in a pricing model customized on the factor’s internal policy.

{kind=link}

The folder’s rating

The results of each analysis contribute to the final rating assigned to the folder. The contribution weight of each analysis (assignor, debtor or transferred portfolio) can be established by the factor, which can thus obtain a risk-adjusted assessment of the entire operation.