Solicited Corporate Credit Rating for CHINA POWER SPA: B1- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of CHINA POWER SPA on the CRA website and the rating assigned to the entity is B1- (first issuance). The analysis revealed how the Company has adequate capabilities to honor obligation and can face adverse and changing economic conditions in the medium and long term.

CHINA POWER S.P.A. operates in the sale of electricity and gas mainly to the Chinese community in Italy. The service is provided in both Chinese and Italian, an element of strong customer loyalty. A further element of loyalty is the use of the WeChat app, widely used within the Chinese community, to contact and communicate with customers. Since its early years, the company has distinguished itself for its sustained growth rates. It was included in the Financial Times ranking of "Europe's fastest growing companies" for the period 2016-2019. The directors and founding members serve as Honorary Chairman and General Manager within the Union of Entrepreneurs Italy China. In 2022, the Italy China Council Foundation recognized the Company as one of the Italian excellences that enhances the trade between Italy and China.

Key Rating Assumptions

The Company presents an adequate economic-financial situation, conditioned only by the worsening of solvency indicators following the increase in liabilities and reduction in shareholders' equity. However, the sustainability of financial indebtedness is not critical as it is correctly supported by operating margins. The balance between short-term sources and uses is correct, stable over the last three financial years, and characterized by liquidity indicators above one. Lastly, the Company shows solid profitability, which is not affected by the trend in revenues caused by the fluctuations in the average price of electricity.

The cash flow analysis confirms that the company has the ability to generate resources through income flow. The financial year 2022 is characterized by a negative operating cash flow, conditioned by the increase in receivables consistent with the expansion of turnover. The analysis of the Italian Central Risk Register shows no critical issues.

The governance structure is appropriate for the company size: the administrative body is formed by the two majority shareholders of the parent holding as directors, flanked by a long-term partner, Mr Caso Fabrizio, as Chairman of the Board of Directors.

The company was founded in 2013 by Song Shengzhong and Jin Marco. In the same year, the 100% parent company SINERGIE PARTNERS S.R.L. was also founded. The shares of the parent company are held 51% by partner Song Shengzhong and 49% by partner Jin Marco. SINERGIE PARTNERS S.R.L. leads a group active in different sectors, within which CHINA POWER SPA plays the role of the main company, providing financial resources to the parent company useful for the development of the other companies.

The Company shows an excellent positioning in terms of turnover, placing it in the 91st percentile of the analysis sample. The positioning of profitability indicators is lower, yet still above the median (71st percentile). In line with the sector median are the values of solvency indicators (44th percentile). The indicators are affected by the company's decision to distribute dividends to the parent company rather than allocate them to reserves to strengthen shareholders' equity. Overall, the peer group shows an adequate state of health: its high levels of leverage are counterbalanced by low levels of financial leverage. Current and quick ratio indicators are sufficient, with values around the unity. The ROE index shows a strong recovery compared to pre-pandemic levels.

The energy sector in Italy is of considerable strategic importance. The operators' market is characterized by a strong granularity, which acts as an important barrier to entry, and by business volume trend strongly anchored to the price of energy raw materials. The Russian-Ukrainian conflict led the country to a necessary reshaping of its supply sources, which was followed by favourable weather conditions throughout 2023. This also contributed to a growth in the contribution of renewable sources to energy production. The medium/long-term picture now appears to be in appreciable recovery and less uncertain.

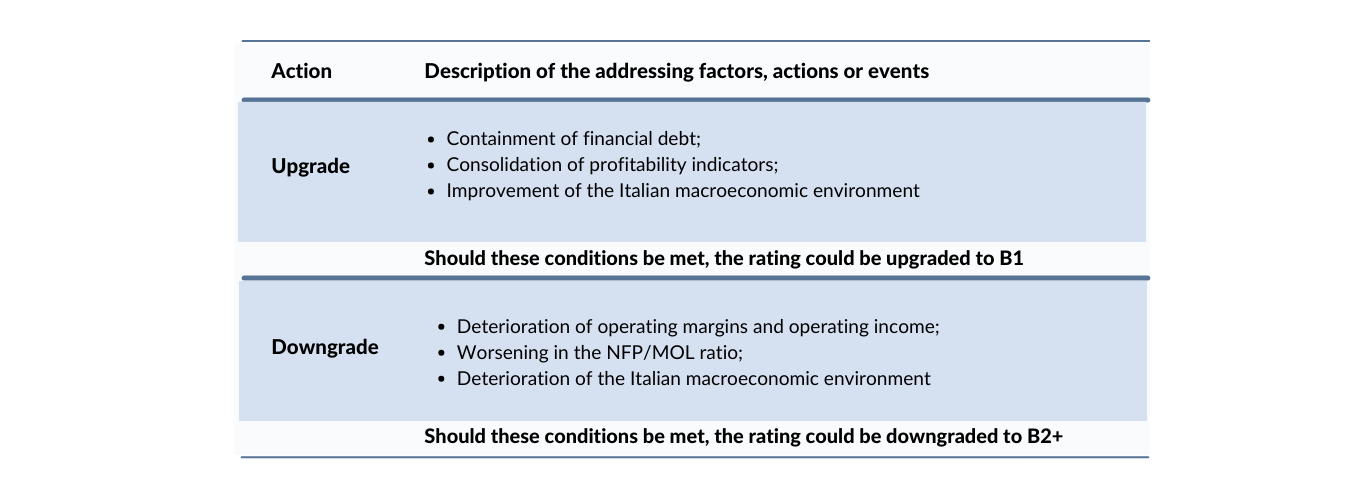

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is a buyer of ancillary services provided by modefinance (preliminary rating). modefinance ensures that such situation does not imply a conflict of interest in the issuance of the present credit rating.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Gabriele Fadon, Rating Analyst

gabriele.fadon@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com