Solicited Corporate Credit Rating for FINECOBANK BANCA FINECO SPA: A2 (Upgrade)

modefinance published the Unsolicited Corporate Credit Rating of FINECOBANK BANCA FINECO SPA on the website, reviewed after the publication of the annual accounts 2022. The rating assigned to the entity is A2 (Upgrade). The analysis revealed it is a very strong bank with strong capability of repaying financial obligations.

FinecoBank Banca Fineco Spa was founded in the late seventies as a company specialized in factoring and leasing operations. In 1999, after several years of M&A, FinecoBank shifted its focus to on online services related to corporate finance, providing highly customized solutions in order to set the standard in a highly competitive environment.

Key Rating Assumptions

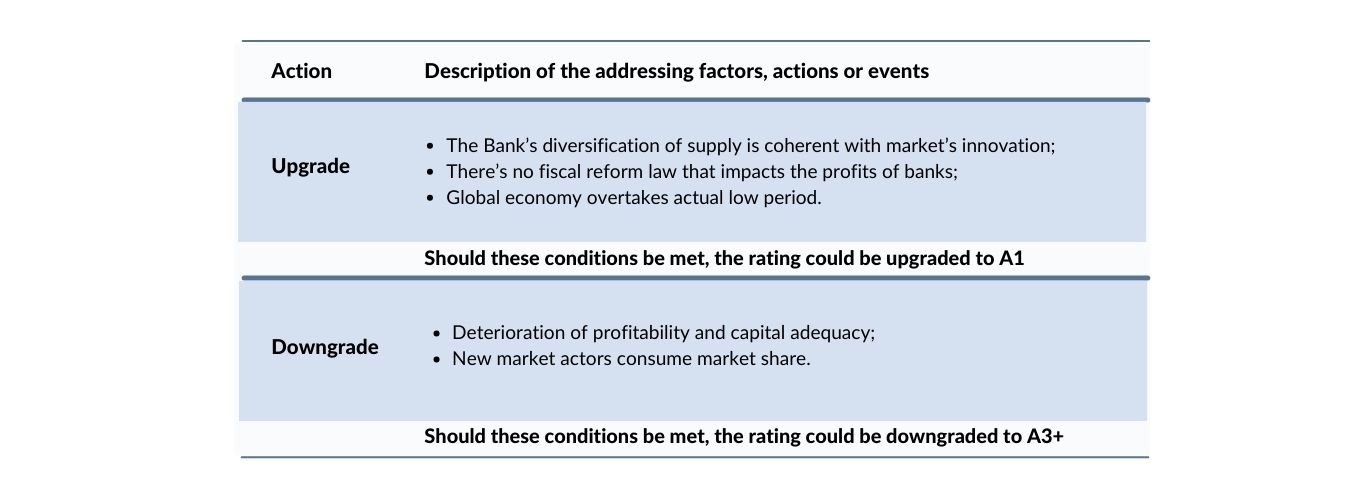

FinecoBank confirms a good economic and financial situation, supported by solid levels of profitability and a high adequacy of regulatory capital. Credit deterioration remains minimal, while operational efficiency is optimal and continues to strengthen.

In 2022, the Bank maintains an exceptionally high level of capital adequacy, with satisfactory performance in lending and profitability. The median value of the peer group for total assets is €6,709 million. The group holds a favorable position (18.91% in 2022) for TCR, surpassing the minimum capital requirements. The peer group recorded a positive trend of ROE over the last three years, with a median value of 7% in 2022. Additionally, the Impaired Loans Ratio for the sector is below the critical threshold, with a value of 0.03 in 2022.

The banking sector turns is one of the traditional pillars of the European economy. Unlike the other sectors, the banking industry seems to have navigated the pandemic phase rather smoothly. However, the main factor of uncertainty currently is the tightening of monetary policy and the phase of high inflation, which may lead to an increase of insolvency cases for both individuals and businesses.

Italian economic growth is expected to further slowdown during 2024, as consumption and investment continue to be strongly influenced by persistently high interest rates, as confirmed by the ECB in mid-December. In the medium to long term, a slowdown in inflationary pressure is anticipated, bringing benefits to both GDP growth and the sustainability of public debt. The recent general elections expressed a solid majority, potentially ensuring the current government’s tenure until the end of this term. In this context, the European Elections 2024 could rebalance the power dynamics within the governing majority. However, the new executive will have to follow the executive agenda set by the previous government in order to successfully implement the post-pandemic recovery plan. There is potential for upward revisions in macroeconomic forecast data.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE for Banks Methodology 2.0 and Rating for Banks Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance however is not in a position to guarantee the accuracy of those information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation. No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary, the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Stefano Chirsich, Rating Analyst

stefano.chirsich@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com