Solicited Corporate Credit Rating for ITALIA POWER S.P.A.: B1 (First Issuance)

modefinance published the Solicited Corporate Credit Rating of ITALIA POWER S.P.A. on the CRA website and the rating assigned to the entity is B1 (first issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

ITALIA POWER S.P.A. is an Italian energy sector’s company since 2016 and, over its first six years of life, has developed a marked lateral diversification, expanding its business to energy efficiency, production and marketing of products related to green mobility, mobile telephony, and clothing. The Company’s fast strategic expansion makes it one of the main ESCo Utilities in Southern Italy.

Key Rating Assumptions

The company ITALIA POWER S.P.A. presents an economic and financial situation characterized by a correct structure of financing sources, with shareholders’ funds covering over 27% of investments. This results in a limited recourse to financial debts, which is consistent with the capital endowment and sustainable based on the margins produced.

Profitability appears to be in appreciable expansion, well sustained both by the growth in the price of energy commodities and by economic benefits of the diversification strategy adopted by management: the effect has been that of a slight growth in profitability indicators, with ROE to be considered of ample sufficiency. In addition, the financial balance appears adequate, with short-term loans largely composed of trade receivables.

With regard to cash flows, a contraction in cash equivalents can be noticed, which nevertheless remain high despite the erosion caused by investments in the new operating HUB and the negative performance of working capital which proved capable of fully absorbing the amount contributed by the new loans taken out. The analysis of credit lines granted to the Company reveals a low incidence of drawn volumes compared to the operating agreement and, at the same time, punctuality in payments.

The governance and control system adopted by the Company is aligned with best practices: the administrative and control body have a collegial form and they are assisted by the work of an auditing company and the presence of a monocratic supervisory body, appointed in compliance with the adoption of 231/2001 model. The corporate structure appears clear in roles, with the majority of shares directly controlled by the entrepreneur Alessandro Esposito.

In comparison with the peer group of reference, the Company's positioning appears solid in terms of size and solvency, while its positioning based on profitability appears close to the 40th percentile, which can be still considered appreciable. The peer group manifests steady growth in its debt levels, although dependence on the financial system continues to be contained. This contributes to the maintenance of appreciable levels of profitability. Moreover, the sector's financial balance is also adequate.

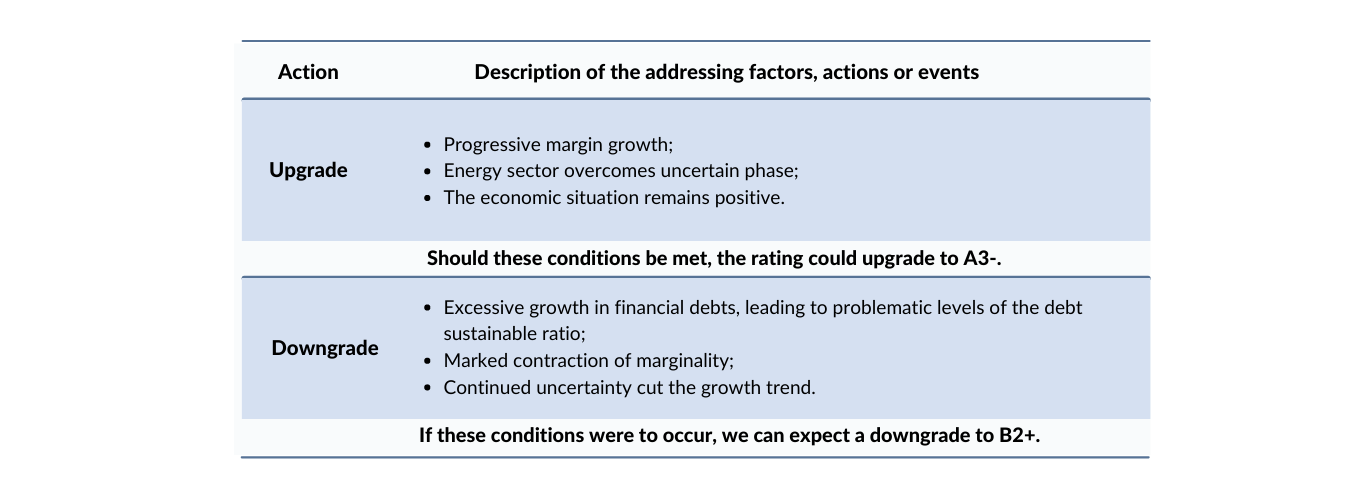

The energy sector in Italy is going through a period of high uncertainty: in the short term, this is caused by strong geopolitical tensions and the need for the Italian government to go to activate alternative sources of supply. The feedback on the macroeconomic front has been a marked rise in inflation, which has eroded economic growth.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Christian Raimondo, Rating Analyst

christian.raimondo@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com