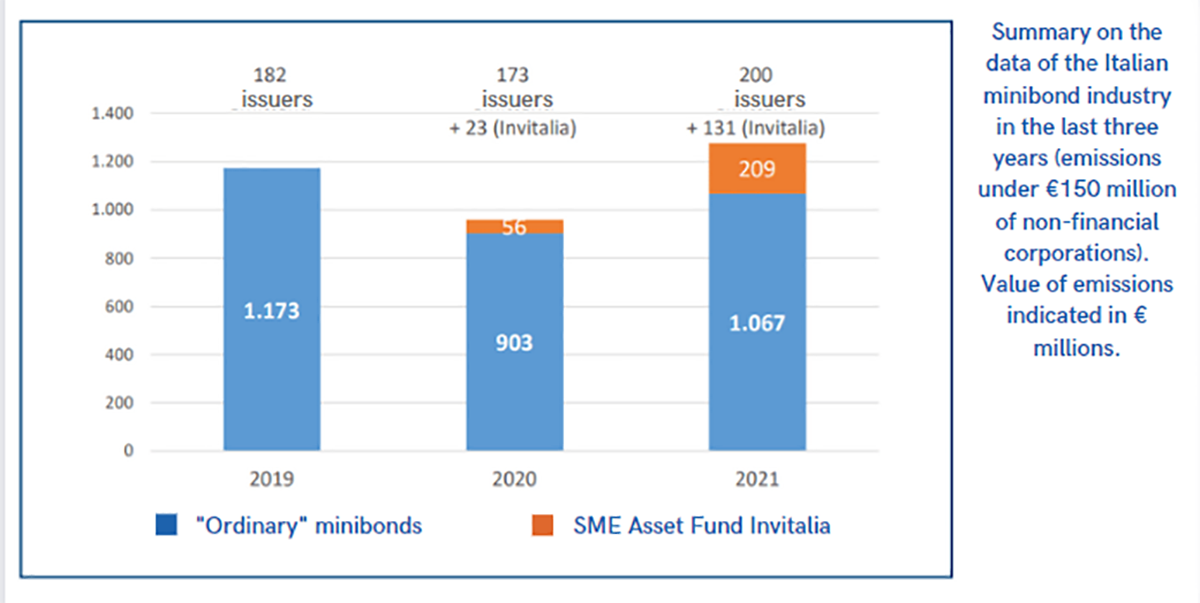

832 Italian enterprises had resorted to minibonds at the date of 31 December 2021; 62,5% of these are SMEs.

This is what emerges from the 8th Italian Minibonds Report issued by the Politecnico di Milano university in March 2022. In the last year, 200 issuer companies were registered, that is 14% more than in the previous year, and the alternative finance leveraged €4,23 billion, 58% more than in the previous analysis.

As much as the funding obtained through issue of bonds is an ever more popular practice for rapidly obtaining liquidity without resorting to a bank credit, many companies are still mistakenly wary of this opportunity, since they consider the issuing of debt securities a difficult to manage tool and suitable only for big businesses. Nevertheless, with the outbreak of the pandemic and the resulting increased need for liquidity and funding on the part of enterprises, the interest for alternative finance has rapidly increased.

{kind=link}

Alternative finance tools: minibonds

Minibonds are medium-long term bond issues of total value lower than €50 million intended to non-listed companies, other than banks and micro-enterprises. Through the issuance of small-size debt securities (hence the name, minibonds), SMEs can raise funds from qualified investors easily and rapidly, without having to resort to a bank loan.

Besides the amount limit, the 2013 Destinazione Italia Decree states that minibonds can be issued only by companies falling under the category of SME, namely with a turnover higher than €2 million and at least 10 employees.

The subscription of minibonds is reserved to professional institutional investors and other qualified entities, which can vary from banks, investment companies, asset management companies (AMC), harmonized management companies, to insurance companies and the like. Investing in SMEs is beneficial for financial institutions since the return is higher and less volatile than other financial tools.

Minibond advantages to win the enterprises' trust

During the two Covid-19 pandemic years, the need for liquidity of companies has increased the use of alternative finance, and this trend is set to continue in the “new reality” we are facing.

The numerous advantages of minibond emissions make them particularly interesting for SMEs. Here are the main ones:

- The loan is stable due to the fact that the duration and refunds are agreed before the placement and are not rectifiable at the discretion of the investor;

- The diversification of funding sources reduces reliance on the banking channel;

- The issuer can choose among three different terms of repayment: the capital can be fully refunded at maturity (bullet), in equal instalments during the whole period (amortizing), or in equal instalments, but only after a first period of 1 or 2 years (grace period);

- They have a medium-to-long-term maturity, even up to 7 years (versus the average of 5 in bank lending), which means stability of credit for a longer period, without the risk of anticipated refund requests;

- They are not reported to the Central Risk Register, thus not precluding access to other funds, in contrast to all exposures towards banks and other financial intermediaries.

How is the minibond emission made and who are the figures that contribute to it?

The issuer and the investor are not the only players that take part in the operation: there are other figures that get engaged in a minibond issuance.

As a first step to be taken, the company needs to contact the advisor. This person will support the enterprise in its initial strategic decision, in the analysis of its business plan and in the definition of the time and mode of issue. Moreover, it is necessary to turn to a legal advisor that will deal with the verification of compliance aspects regarding contracts and regulations of the loan.

Meanwhile, the arranger manages the placement of bonds on the market and the movement of funds, while finding potential investors. In fact, the arranger plays the role of financial coordinator.

An extremely important figure in the minibond emission process is the Credit Rating Agency. It provides potential investors with company information and with the development of its business, thus expressing independent judgements on the state of health of the issuing company.

Initiatives for minibond emissions: Basket Bonds

There is only one crucial point to mention when dealing with minibonds. It is possible to undertake the basket bond path for their issue. Basket bonds are bond portfolios that gather emissions of a group of companies, usually united by a strong thematic or territorial connotation.

In order to partake in a basket bond operation, the enterprise can submit its application on dedicated portals. After that, the arranger will select the enterprises that will form the portfolio and then create a Special Purpose Vehicle (SPV) that will buy the bond, composed of a pool of securities.

Among the key Basket Bond initiatives active in Italy, it is important to point out Basket Bond Loan and Basket Bond Mezzogiorno, both launched by Elite in collaboration with Banca Finint, as well as Garanzia Campania Bond.

As the first Fintech Credit Rating Agency (CRA) in Europe, as well as the most active one in Italy as far as minibond-related rating issuance is concerned, modefinance is capable of evaluating any SME that chooses to issue minibonds in order to finance its projects and investments. Thanks to our products and advanced technologies, we can evaluate our clients’ state of health by providing an efficient and reliable credit rating, thus facilitating access to capital and making investors’ activities easier and safer.